Effective January 1, Mauser Packaging Solutions has expanded the U.S. 401(k) retirement savings options for nonunion employees by adding a Roth 401(k) option. This new option provides additional flexibility for employees to choose a plan that best meets their individual needs.

This new Roth 401(k) option is being added to the U.S. Vanguard plan and excludes the Puerto Rician plan.

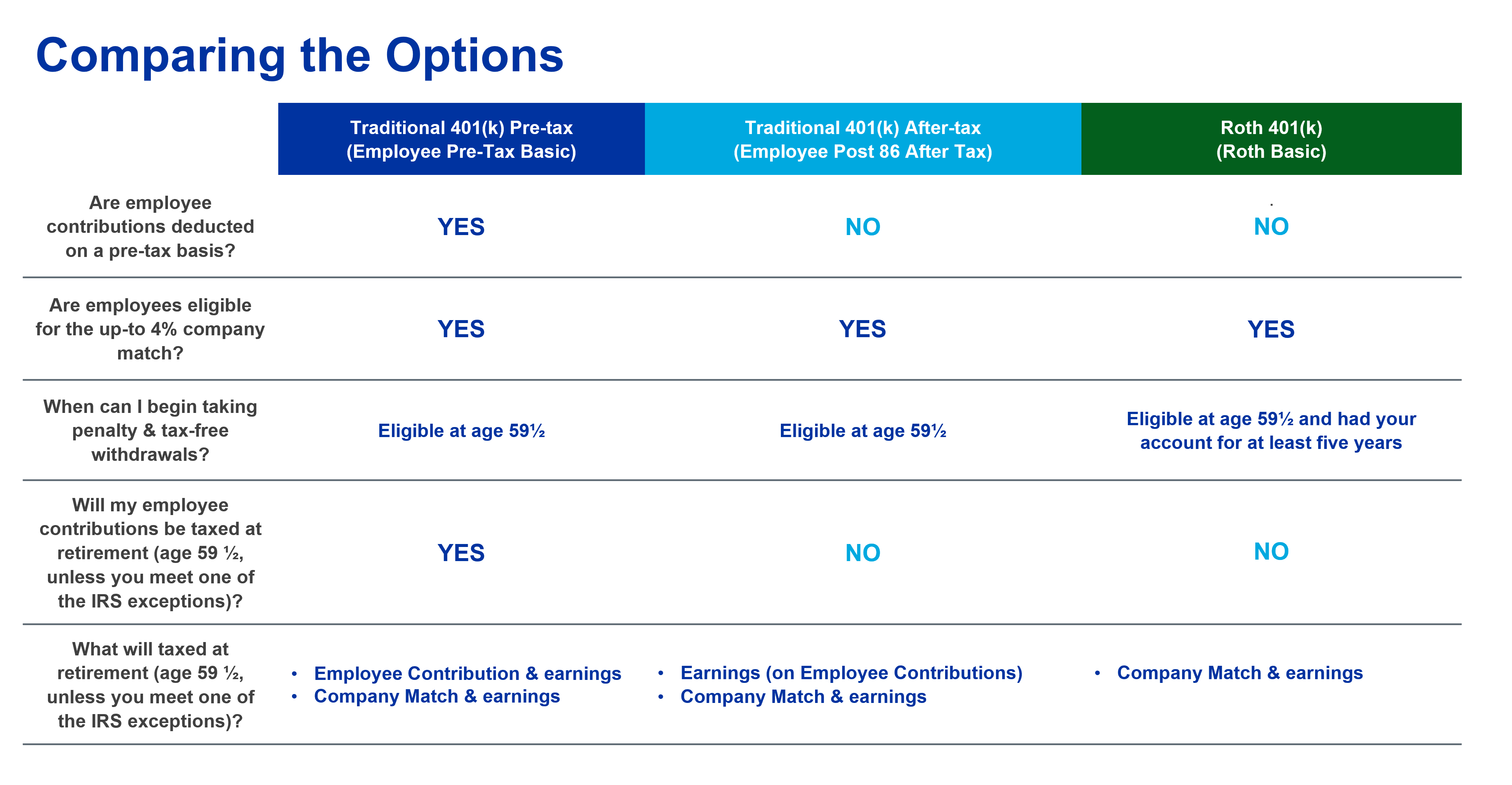

The new Roth 401(k) option offers many of the same features of the traditional 401(k) such as administration by Vanguard, investment opportunities, eligibility after one year of service to receive a Mauser match of 100% on the first 4% of eligible compensation contributed, and subjectivity to contribution limits1. Contributions are deducted via payroll deduction after earnings have been taxed. However, employee contributions and any growth on employee contributions through the plan are tax and penalty free during retirement. Taxes are only applied to the company match and earnings on the match. Also, with a Roth 401(k), the account must be held for at least 5 years before it can be withdrawn without penalty.2

The traditional Mauser 401(k) retirement savings option, also administered by Vanguard, will continue to be offered without change. With a traditional 401(k), contributions are deducted from your paycheck, are subject to contribution limits1, and participants become eligible after one year of service to receive a Mauser match of 100% on the first 4% of eligible compensation contributed. This more traditional retirement savings option is comprised of two components – 401(k) Pre-tax and 401(k) After-tax. The main difference between these two options is when taxes are applied.

There are many factors to consider when determining which plan type and option is best for each individual person. When you are choosing between a traditional 401(k) and a Roth 401(k), you should consider whether you want a tax advantage now or later in life and which option may provide the greatest tax benefit. Before you make any decision about Roth contributions, consider consulting a professional tax advisor about your individual situation.

Mauser is committed to providing a robust 401(k) retirement plan with options that best meet the individual needs of each employee. We recognize your future is just as important as your present and additional options for retirement saving will assist you in planning for the future that is right for you.

1Contribution limits are set by the IRS on an annual basis. For 2024,

-

- 401(k) Pre-tax and Roth 401(k):

- $23,000 if under age 50 in 2024

- $30,500 if age 50 or older in 2024

- 401(k) Pre-tax, 401(k) After-tax, and Roth 401(k):

- Subject to overall contribution limit of $69,000 in 2024, inclusive of pre-tax 401(k), Roth 401(k), after-tax 401(k), and any employer contributions.

- 401(k) Pre-tax and Roth 401(k):

2 Traditional and Roth 401(k) accounts are accessible for withdrawal at age 59½ penalty free. Traditional 401 (k) accounts can be withdrawn regardless of how long the account has been held. Roth 401 (k) accounts must be held for 5 years prior to withdrawal to avoid penalty.

Additional Resources

Employees are encouraged to access available Vanguard resources or consult a tax professional for personal retirement savings and investment advice.

View the U.S. 401(k) Retirement plan – Nonunion: Expanded Retirement Savings Option presentation deck for more detailed information.

Access Vanguard.com via MauserNOW/Resources.

- Visit My Financial Wellness to:

- Take Control of your Finances

- Use Learning Resources

- Set Goals

- Explore Webinars

- Visit Manage my Money to:

- Contact a Vanguard Financial Advisor

- Set Goals

- Explore Webinars