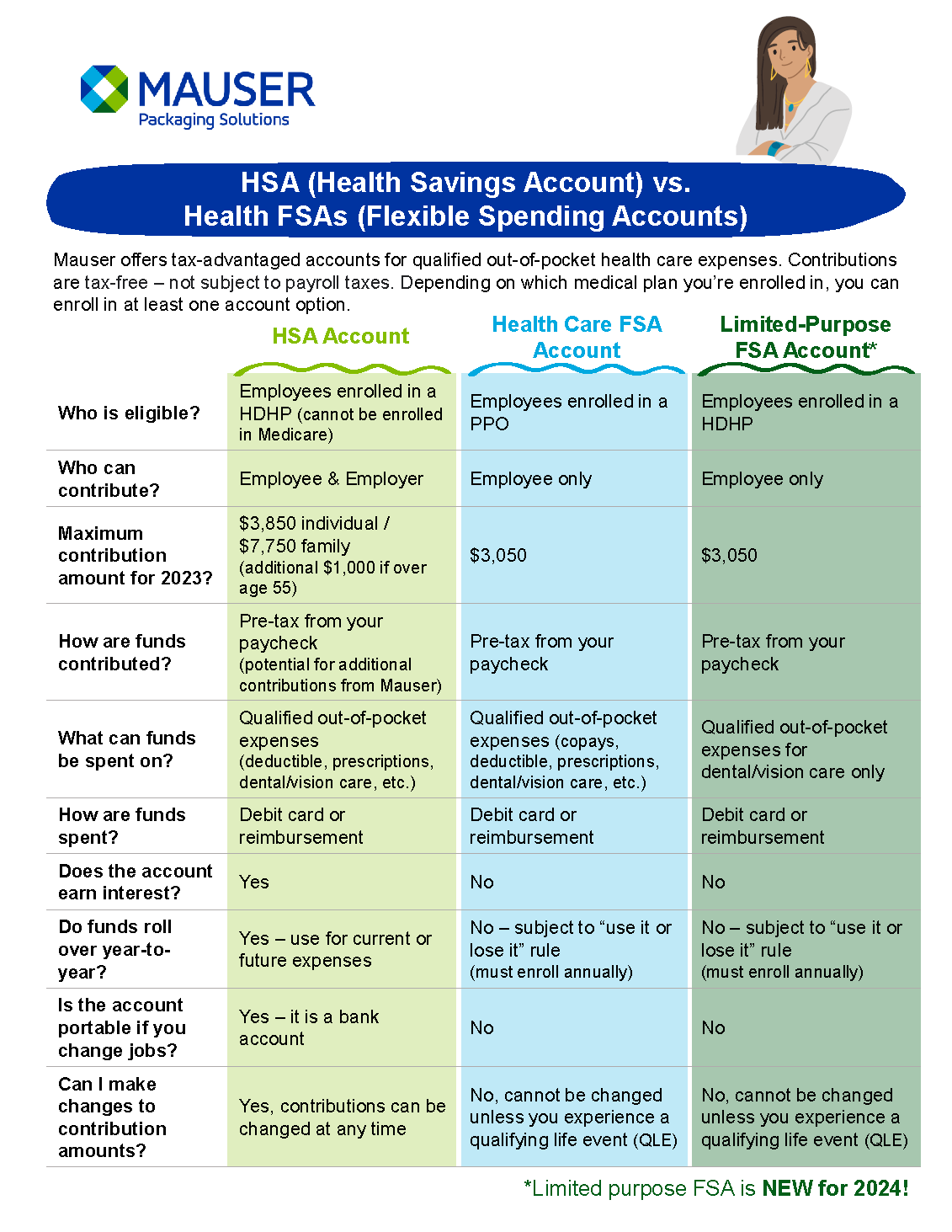

Mauser Packaging Solutions offers tax-advantaged savings accounts for qualified out-of-pocket health care expenses. Contributions are tax-free meaning contributions are not subject to payroll taxes (i.e., you don’t have to pay federal, state or Social Security taxes on this money). Depending on which medical plan you’re enrolled in, you may have access to a Health Care Flexible Spending Account (FSA), Health Savings Account (HSA) and/or a Limited-Purpose FSA Account (LPFSA).

Let’s dive a little deeper into what FSAs and HSAs are, how they work, and what you can use the funds for. Don’t miss out on your benefits – knowing these differences may help you know how to use these accounts to your advantage.

Health Care Flexible Spending Account (FSA)

What is a Health Care FSA?

A Health Care Flexible Spending Account (FSA) is designed to help employees set aside money to pay for out-of-pocket health care costs during the plan year. Contributions to an FSA provide a tax break since they are not subject to payroll tax.

Eligibility:

Only employees enrolled in the PPO medical plan or who waive medical coverage through Mauser are eligible to enroll in the Health Care FSA plan.

How do FSA's work?

- Employers set the maximum amount that you can contribute; however, it can’t exceed the annual IRS limit ($3,050 in 2023; not yet published for 2024).

- An FSA is not a savings account. If you leave your job, you can’t take your FSA with you.

- If you don’t use the full amount you’ve elected to contribute by the end of the calendar year, you could lose, or forfeit, your FSA dollars.

- You must enroll annually during Open Enrollment, so you’ll have to decide how much money you want to set aside for the year.

- Using your FSA is easy. Your FSA comes with a handy debit card, which makes it easy to pay for services from your FSA. Other options include:

- Automatic payment-Claims from UHC Medical and Rx will automatically rollover and reimburse you from the FSA.

- Online claim form-Easily submit claims on myuhc.com to get reimbursed from your FSA.

- Direct deposit-UHC can reimburse your money directly into your personal bank account.

How can I use the money in my health care FSA? What can I buy?

You can use your FSA for qualified medical expenses and services, as defined by the Internal Revenue Service. What The list of qualified medical expenses is extensive, but some of the more common expenses and services include:

- Deductibles

- Copayments

- Prescription medication

- Over-the-counter medication

- Vision care, including prescription eyeglasses and contact lenses

- Thermometers

- First-aid kits

- Hearing aids

- Diabetic supplies

- Chiropractic care

Health Savings Account (HSA)

What is a HSA?

A Health Savings Account (HSA) allows employees to set aside money to pay for out-of-pocket health care costs at any time. These accounts can grow over time through interest and investment earnings. Contributions to an HSA provide an immediate tax break since they are not subject to payroll tax. Additionally, these the interest and investment earnings on these accounts are not taxed and withdrawals for qualified medical expenses are not subject to income tax. With this triple tax savings, an HSA facilitates savings today, tomorrow, and even through retirement.

Eligibility:

Only employees enrolled in a high deductible health plan (HDHP), also known as an HSP/HSA are eligible to contribute to an HSA account.

How do HSA's work?

- Each year, the Internal Revenue Service (IRS) sets contribution limits for health savings accounts (HSAs). 2024 HSA contribution limits:

-

- An individual (with employee only coverage) and employer can contribute up to $4,150.

- An individual (with family coverage) and employer can contribute up to $8,300.

- Eligible individuals, 55 or older, can contribute an additional catch-up contribution of $1,000 per year.

- The money in your HSA is always yours. There is no “use-it-or-lose-it” rule. All amounts in your HSA are fully vested, and unspent balances in accounts remain there until spent. Your account is also portable meaning your money stays put even if you:

- Change jobs

- Change medical coverage

- Become unemployed

- Move to another state

- Get married or divorced

- For Mauser employees, you must enroll annually during Open Enrollment – contribution designations do not automatically carry over from year-to-year. However, you can change or end your election at any time during year by logging into the Mauser Benefits Portal (Alight).

- With Optum Bank, using your HSA is easy. Your HSA comes with a handy debit card, which makes it easy to pay for services from your HSA. You can also reimburse yourself by submitting a Reimbursement Form or use the Pay a Bill feature to pay your provider.

How can I use the money in my HSA? What can I buy?

Use your HSA to pay for qualified medical, dental, vision, hearing, and prescription expenses, plus copays, coinsurance, and hundreds of eligible items and services.

Limited-Purpose Flexible Spending Account (LPFSA)

* NEW for 2024!

What is a LPFSA?

A Limited Purpose Flexible Spending Account (LPFSA) is designed to pair with an HSA and is a tax-advantaged account that lets you set aside pre-tax money to pay for eligible dental and vision expenses.

Like the Health Care FSA, a LPFSA can be used for eligible dental and vision expenses incurred during the plan year but remember that it is a “use-it-or-lose-it” account.

Eligibility:

Only employees enrolled in a high deductible health plan (HDHP), also known as an HSP/HSA and are enrolled to contribute to an HSA are eligible to contribute to an LPFSA account.

How do LPFSA's work?

- Employers set the maximum amount that you can contribute; however, it can’t exceed the annual IRS limit ($3,050 in 2023; not yet published for 2024).

- An LPFSA is not a savings account. If you leave your job, you can’t take your LPFSA with you.

- You must be enrolled in an HDHP and contribute to an HSA to have an LPFSA, but the choice to use both is up to you. Electing to use both accounts in tandem can help save money each year.

- If you don’t use the full amount you’ve elected to contribute by the end of the calendar year, you could lose, or forfeit, your LPFSA dollars.

- You must enroll annually during Open Enrollment, so you’ll have to decide how much money you want to set aside for the year.

- Using your LPFSA is easy. Your LPFSA comes with a handy debit card, which makes it easy to pay for services from your LPFSA. Other options include:

- Online claim form: Easily submit your claims on myuhc.com to get reimbursed from your LPFSA.

- Direct deposit: UHC can reimburse your money directly into your personal bank account.

How can I use the money in my LPFSA? What can I buy?

LPFSAs can be used to cover the costs of qualified dental and vision expenses. Here are some examples of out-of-pocket expenses you can use an LPFSA for:

- Braces

- Contact lenses and solution

- Dental services

- Dentures and bridges

- Diagnostic services

- Eye exams

- Fillings

- Laser eye surgery

- Office visits (dental and vision)

- Oral pain products

- Sunglasses (Rx)

- Teeth cleaning

- X-ray fees (dental)

Resources

- Click here for more information on FSAs.

- Not sure how much to put in your FSA? Click here to use UHC’s FSA Savings Calculator.

- Click here for more information on HSAs; see page 6 for Eligibility Information.

- Not sure how much to put in your HSA? Click here to use Optum’s HSA Savings Calculators.

- For a complete list of eligible expenses, click here to review Internal Revenue Service (IRS) Publication 502.